IRS Releases Inflation Adjustments for 2021

- monica4867

- Nov 6, 2020

- 4 min read

Article Highlights:

Standard Deduction

Transportation Fringe Benefits

Retirement Plans Contribution Limits

SIMPLE Retirement Accounts

IRA Contribution Limits

Health Flexible Spending Accounts

Education Credits

Estate Tax Exclusion

Annual Gift Exclusion

Sec 179 Expensing Deduction

Foreign Earned Income Exclusion

Alternative Minimum Tax

Adoption Credit

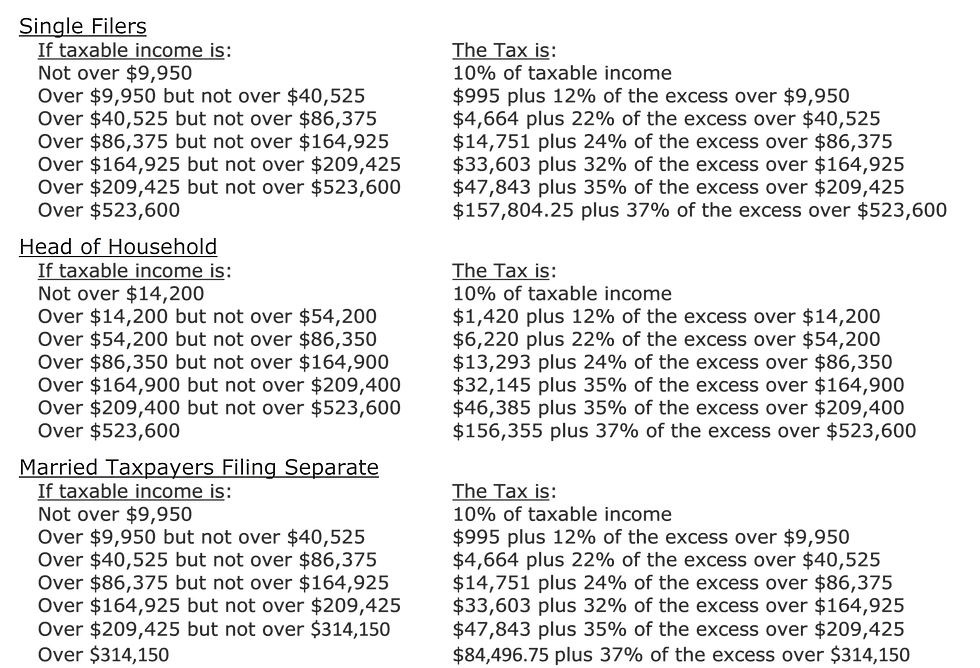

Tax Rate Schedules

To cope with inflation, the tax code requires the IRS to adjust the tax rates, standard deductions, and a variety of other tax related numbers each year. Due to the relatively low rate of inflation from 2020 to 2021 (at least according to the calculation method prescribed by law for this purpose), several categories had no or only a slight change. The following is a summary of the most commonly encountered items for 2021.

Standard Deductions – The standard deduction consists of a filing status-based basic amount and additional amounts for elderly and blind filers (and their spouses). The additional amounts do not apply to dependents. The 2020 and 2021 amounts are compared below.

Qualified Transportation Fringe Benefits - Qualified transportation fringe benefits for transit passes, commuter transportation and qualified parking provided by an employer are excluded from an employee’s income up to the amount of the inflation adjusted dollar limitation, which remains unchanged and will be $270 per month for 2021.

Retirement Plans Contribution Limits - The limit on contributions by employees who participate in Sec. 401(k), Sec. 403(b), most Sec. 457 plans, and the federal government’s Thrift Savings Plan remains unchanged and is $19,500 for 2021. The catch-up contribution limit for employees age 50 and over also remains unchanged at $6,500.

SIMPLE Retirement Accounts - The contribution limit for SIMPLE retirement accounts remains unchanged and is $13,500 for 2021.

IRA Contribution Limits - For IRAs, the limit on annual contributions remains unchanged at $6,000 for 2021 and the additional catch-up contribution limit for individuals age 50 and over is $1,000. This limit applies to the combination of traditional and Roth IRAs. However, there are additional limitations that apply to both traditional and Roth IRAs.

Traditional IRA – Typically contributions to a traditional IRA are tax deductible unless the taxpayer is also an active participant in an employer plan in which case the deductibility of the contribution is phased out for higher income taxpayers. The phaseout thresholds have increased somewhat for 2021.

· Roth IRA Contributions – Roth IRA contributions are phased out for higher income taxpayers whether or not they actively participate in an employer’s plan. The AGI thresholds limiting Roth IRA contributions have been increased slightly for 2021.

Health Flexible Spending Accounts – These plans are established by employers to reimburse employees for health care expenses and are usually funded by employees through salary reduction agreements. Qualifying contributions to and withdrawals from FSAs are tax-exempt. For 2021, employee salary reductions for contributions are limited to $2,750, unchanged from 2020. However, the funds must be used during the year or they are lost, except for a small carryover amount which has increased from $500 in 2020 to $550 in 2021.

Education Credits – Both the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) are phased out for higher income taxpayers. However, only the phaseout for the LLC is inflation adjusted. For 2021 the LLC phaseout threshold for joint filers is $119,000, up from $118,000 for 2020. For other taxpayers the 2021 phaseout starts at $59,000, but a married individual filing a separate return can’t claim this credit.

Estate Tax Exclusion – The amount of the estate tax exclusion for a decedent passing away in 2021 has increased to $11.7 million, up from $11.58 million in 2020.

Annual Gift Exclusion – This amount is unchanged, so the first $15,000 of gifts (other than gifts of future interests in property) to any person in 2021 is exempt from the gift tax. 2021 is the fourth consecutive year that this exclusion has been $15,000.

Sec 179 Expensing Deduction – The Internal Revenue Code allows a business taxpayer to expense, limited to taxable income from all of the taxpayer’s active trades or businesses, rather than depreciate, certain property used in business. For 2021 the maximum is $1.05 million ($525,000 for married taxpayers filing separate) up from $1.04 million in 2020. The phaseout threshold based on the cost of Sec 179 property also increased, to $2.62 million, up from $2.59 million.

Foreign Earned Income Exclusion – U.S. citizens or resident aliens who live and work abroad who meet certain qualifications may be able to exclude from U.S. income foreign earnings not to exceed an annual maximum amount. In addition, these taxpayers may be able to exclude or deduct certain foreign housing cost amounts. For 2021, the maximum foreign earned income exclusion is $108,700, up from $107,600 in 2020.

Alternative Minimum Tax (AMT) – The AMT is an alternate way of computing an individual’s income tax and applies if the AMT is greater than the regular tax. Generally, the AMT comes into play when an individual has a large amount of specified tax preferences and deductions. There are sizable exemption amounts based on filing status, and they have increased for 2021.

These exemption amounts phase out for higher income taxpayers. The thresholds for the phaseouts are:

Adoption Credit - The maximum credit allowed for adoptions in 2021 is equal to qualified adoption expenses incurred up to $14,440, a $140 increase from $14,300 for 2020.

Tax Rate Schedules – Each year the tax rate schedules are also adjusted for inflation. The following are the schedules for 2021.

Optional Auto Mileage Rates – The optional vehicle mileage rates for 2021 will not be released until later in the year or early in 2021.

If you have any questions, please give the office a call.

Comments